![]()

The purpose of investing and hence building wealth is to ultimately give yourself the power and security of choice. Whether that choice later in life is to separate from the ADF and start your own business; put your kids through a top private school; assist relatives with life-changing surgery; buy a few expensive toys or simply do more volunteering – the reality is the power that choice provides can never be under-estimated.

Because we are investors, our TWO-50-TEN™ strategy is one that has been tried, tested and proven. Its aim is simple – to build a sizeable asset base over time that will eventually become self-funding. This means that the rental yield covers all outgoings in holding the property whilst leaving surplus income to service lifestyle and ability to draw against future cyclic capital growth.

What is gearing? (ACQUIRE)

The term gearing in this sense means you have borrowed money in order to invest with the intent of generating rental income. If the rental income is more than the outgoings (loan interest, insurance, council rates etc.) then you are earning extra income and are therefore positively geared. If the outgoings are more than the rental income then you are negatively geared.

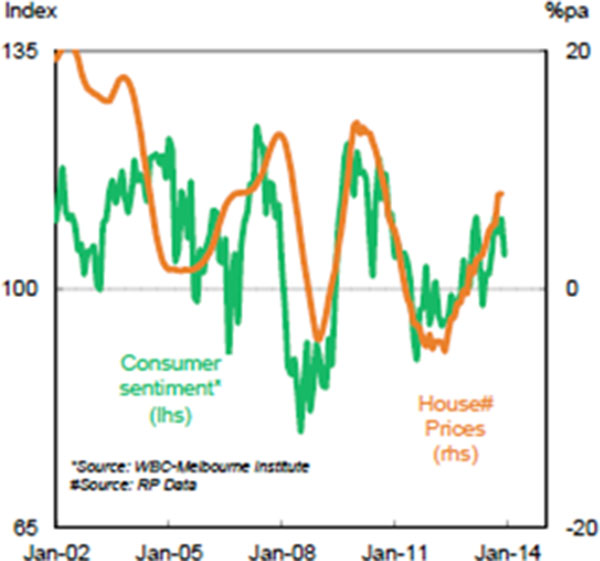

As time goes on the value of your portfolio can reasonably be expected to increase annually due to various economic factors such as supply and demand, the availability of credit, consumer sentiment, low unemployment and of course inflation. This increase in portfolio value (also known as equity) is what provides the deposit to further acquire more investment properties.

Once you have acquired your critical mass of assets, the next stage of the strategy is to start reducing your debt – otherwise known as Loan-to-Value Ratio (LVR).

How do I reduce that? (CONSOLIDATE)

The reduction in LVR assists in compounding the growth of your net worth. This has the effect of increasing your net rental return and therefore your serviceability.

LVR can be reduced in the following ways:

• Cease (or slow down) acquiring further properties so that while the value of your portfolio keeps rising, your loans remain much the same;

• Pay off some debt using windfalls or superannuation (MSBS or industry-super lump sum);

•Reduce debt by paying principal and interest as opposed to interest-only;

•Add value to the property by way of a renovation, extension or subdivision; or

• Sell down a property or two.

The first phase however always involves building a substantial and quality asset base!

So do I live off the rental income?

No. It’s important to understand that the intent of this strategy is not for you to live off the rental income initially. It is designed for you to access and live off a strong combination of growing equity and rental income. Of course this requires your properties to always increase in value, and this can be reasonably expected to occur provided you have bought the right property in the right area and at the right price. This is a property that has a level of scarcity – meaning it will be in continuous strong demand by owner occupiers (to keep pushing up the value) and tenants (to help subsidise your mortgage); in the right location (one that has outperformed the long term averages with strong local economic fundamentals) and at the right time in the property cycle which is now in the majority of markets. This is a combination of market fundamentals and economic cycles at play. Remember – right property in the right area and at the right price.

The key thing about well-located residential property (land specifically) is that it is almost recession-proof. Housing is of course necessary for survival and land is a necessary pillar of any economy. A good way to think of your investment property is that the house or building is the business that generates the cash-flow to sustain your holdings. As a residential property investor, you are in the business of providing shelter. The land or location is the actual wealth-holding that increases in value over time. Simply put – the dwelling supplies cash flow (rent) and the land/location supplies equity (capital increase).

What’s a realistic and achievable example?

Go forward 10-15 years from now and envision you own your own home plus $5-million of well-located investment properties.

If you had a typical 80% Loan-to-Value Ratio, you would most likely be negatively geared meaning the shortfall would have to be funded from other income sources such as your salary or tax-return or both.

If you had no debt against your property portfolio (0% LVR) you would have positive cash flow, but you would have foregone the benefits of leverage or gearing. In this case you have not used other people’s money to ‘lever’ or ‘gear up’ into a bigger portfolio and have therefore wasted time and the effects of compounding in your favour.

Somewhere in the middle, perhaps with a 50% LVR, your property portfolio will be self-funding. You may even have a little cash-flow left over, but definitely not enough to live on.

If you think about it, it will be much easier and take less time to amass a $5-million property portfolio with $2.5-million of debt (50% LVR) than the same size portfolio with no debt (0% LVR).

You could then approach your lender and explain you hold a self-funding property portfolio that isn’t reliant on your working income and in fact, there’s a little cash left over for serviceability. You may then apply for an extra $100,000 loan (equity release) so in this case you’re increasing your LVR slightly to 52%.

The good news is that you don’t have to pay tax on this money because it’s not income. But you would have to pay interest, which won’t be tax deductible if you use the money for personal use.

This means that after the interest payments (7%) you’re left with around $93,000 to utilise or live off. If this was $100,000 in earned income from a day-job, you’d be up for $26,988 in tax leaving only $73,012 to utilise. (Source: ATO 2014-15 tax rates).

How is it self-sustaining? (SUSTAIN)

At the end of the year you may have ‘burned through’ your $100,000; but in a good year with 10% annual growth, your $5-million property portfolio would increase in value by $500,000. At a conservative 4% growth rate this equates to $200,000. You also would expect your rents to also have increased over the year because your properties have increased in value.

Yes, you may have used the $100,000 you initially extracted, but because your portfolio has risen in value along with rents, your LVR is less at the end of the year than the beginning, so you finish off the year wealthier than you began it. At 10% growth your new LVR would be 47.2%. At 4% growth you would be back at 50% LVR despite having extracted $100,000 a year earlier. Because your rental returns are based on the current market value of your properties and your loans are based on a value equal to 50%, you will find that you will also be in a healthy cash-flow position.

You also have the added benefit of increased capital protection, because at 50% LVR, the Australian residential property market would have to fall by more than 50% before you find yourself in a negative-equity position. With this strategy you are working towards a powerful combination of cash-flow, capital growth and risk mitigation in an asset class so crucial to society. What you’ve truly got now is a self-sustaining, risk-mitigated portfolio giving you the power of choice.

Post-GFC the equity-release strategy became harder for higher LVR portfolios. Therefore the key lies in building your asset base with quality stock, lowering your LVR once critical mass is achieved and demonstrating serviceability.

Needless to say you can’t achieve this overnight and all property investment decisions must be made with reference to the grand 18-year real-estate cycle. It does takes time to build a substantial asset base and a comfortable loan-to-value ratio. But if you responsibly take advantage of the powerful effects of leverage, compounding and time – you will be pleasantly surprised at its simplicity.

This is a proven strategy that takes advantage of the globalised inflationary-based, fiat-currency economy that we live in today. Zero-interest rate policy (ZIRP) in the US, Japan and Europe and Quantitative Easing (QE) also in the US are measures employed by their respective central banks to promote inflation.

Possessing a large enough asset base that hedges against inflation is crucial to long-term personal and family wealth.

What about risk?

Of course this strategy depends on the growth in your property portfolio and your ability to ride out the property cycles. This means that as you build your asset base by building brand-new properties in fundamentally strong high-growth locations, you will need a risk-management plan to see you through the market peaks and troughs that will be experienced.

We do know that over the next 10-15 years there will be both good and challenging times ahead. There will be peri ods of high interest rates and periods of lower interest rates. And we’ll have periods of strong economic growth and periods of downturn. Savvy investors count on the good times but are prepared for potential downturns by having an asset protection plan as well as a finance and tax strategy that ensures their structures are as efficient and effective as possible.

ods of high interest rates and periods of lower interest rates. And we’ll have periods of strong economic growth and periods of downturn. Savvy investors count on the good times but are prepared for potential downturns by having an asset protection plan as well as a finance and tax strategy that ensures their structures are as efficient and effective as possible.

As long as each property has been assessed appropriately for potential cash flow, capital growth and risk – you can and should be confident in your acquisition. The key to successful property investment is to begin with the end in mind. You need to define and be absolutely clear with what it is you want to achieve in terms of finances and lifestyle. Our team are experienced in helping you define your goals and instigating a property investment plan that will ultimately help you achieve them.

Simply put, the three distinct phases are:

ACQUIRE – CONSOLIDATE – SUSTAIN

What phase are you in..?

If you’ve got any questions, would like to explore property investing further or simply want to receive our regular Short Sharp & Sweet insights – please get in touch using the form below or email us directly info@defencewealth.com.au and say G’day!

Continue to Property

Continue to our Service Offering

Important information: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. For this reason, any individual should, before acting, consider the appropriateness of the information, having regard to the individual’s objectives, financial situation and needs and, if necessary, seek appropriate professional advice.