G’day All,

What a great year 2021 has been for Aussie property!

Official cash rate is still at 0.1% – this means the velocity of money flowing through the economy is still considered too low. The RBA don’t anticipate needing to increase this until 2024, but it will all depend on what inflation, wages and unemployment does between now and then.

So when will mortgage rates rise?

CBA and Westpac are tipping they’ll rise a year earlier in 2023. This is because of the huge amounts of pandemic stimulus the government has pumped into the economy. Due to rolling lockdowns, people haven’t had the chance to travel or spend as they would normally. As a result, over $200 billion is estimated to be sitting in savings accounts that will eventually find its way into the economy and ultimately property (land) prices.

This will see inflation and wages increase meaning interest rates will have to rise in order to prevent the economy from overheating. We’ll be keeping an eye on inflation and wages growth going forward.

What about the recent APRA restrictions?

From November, banks must assess your serviceability with a 3% buffer (currently 2.5%) ie: if the bank’s standard variable rate is 3.5%, you’ll be assessed for ability to repay at 6.5% P&I.

APRA are also considering introducing debt-to-income (DTI) ratios capped at 6x, meaning for a person earning $100k gross, the max debt they can hold is $600,000. This isn’t in play yet, however if it is introduced, it will constrain diligent and responsible investors from expanding their wealth base.

It also risks creating a bigger wealth gap between those with and without property. If for instance you owned two investment properties, your PAYG salary plus total rental income would equate to a higher lending cap and therefore ability to expand your asset base.

A person without assets would see their lending capped based on their salary amount only until rental income could be demonstrated.

Tax Update

Although still in draft state, a tax ruling permitting interest deductions for the construction component of lending for an investment property has been issued by the ATO. The land component of lending still cannot be claimed until the property is built and genuinely available for rent.

For clients who have recently begun the building process or built within the last two years, it’ll be worthwhile discussing this with your accountant, or let us know if you’d like us to assist with your tax affairs if not already.

18.6-year land cycle

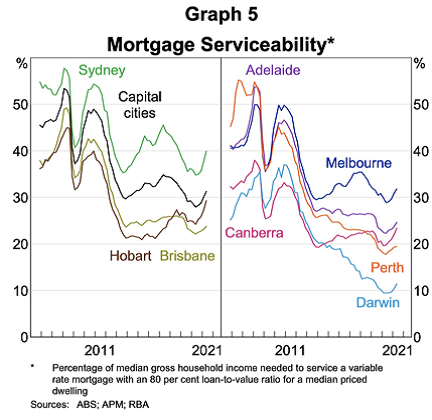

As touched on in previous updates, we’re now firmly into the second-half of the real-estate cycle. Key industries for this stage are commodities, agriculture and defence. When combined with high affordability as seen in the graph below (percentage of median income required to service a median mortgage), this broadly equates to the markets of Perth, Brisbane, Adelaide, Darwin and major regionals such as Toowoomba.

This is also a global phenomenon as property values in the US and UK are experiencing similar gains.

Going forward…

If you’re considering investing for the first time or looking to add to your portfolio, I’d suggest now and the next 24 months (circa late 2023) is the window of opportunity. We expect to enter the winners-curse phase from mid-2024 onwards, and although good purchasing may still be possible, extra diligence and prudence will be needed.

Please drop us a line if you’d like to explore your lending and/or property investment options and begin setting your future-self up now.

Strategy

The Defencewealth strategy of TWO-50-TEN™ is based on acquiring a $2 million portfolio at 80-90% LVR over a 6-8 year timeframe. Once acquired we work to reduce the LVR to 50% over the next 4-7 years using a combination of capital growth, offset accounts and principal repayments. Once at 50% LVR, you will have some serious financial options but it will take time (min 10-15 years) to achieve. The new property packages we recommend are considered investment-grade based on experience and results and are selected for their balance in anticipated cash flow, capital growth and risk.